Graph P**n Exponential

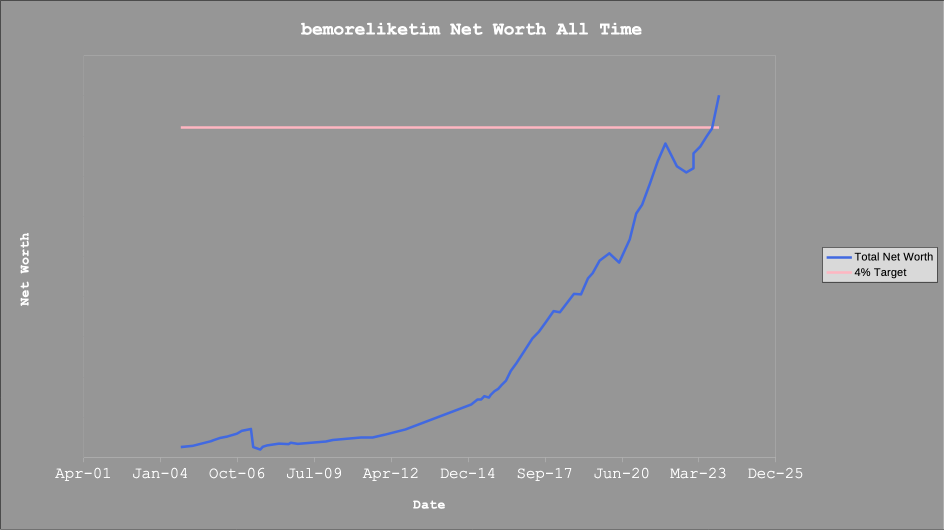

It may come as no surprise that I keep a spreadsheet of my net worth. The thing is, although I’ve got figures going back 20 years, I’ve only been keeping an eye on a net worth chart with data for the last 10 or so. A few days ago, it occurred to me to graph the whole dataset. Note this isn’t the whole dataset because I lost some of the early numbers (1998-early 2000s), but they would be scraping along the bottom of this chart.

That is real life exponential growth in action.

A month or two ago, a couple of posts on exponential growth were doing the ‘social media’ rounds. I love them because, like optical illusions, they were designed to exploit and illustrate glitches in the human system. There’s the one where you have a choice between a penny that doubles every day for a month, or £1,000,000 in your pocket right now. There’s the other telling the French riddle of the lily pond with a single lily on day one, that doubles in quantity every day. If the pond is covered on the 30th day, when is it just half covered? For the answers, you should definitely take the 1p doubling every day as you’ll end up with somewhere between £1,342,177.28 on a 28 day month, or for a 31 day month . . . and this still bends my brain . . £10,737,418.24. In less exciting news, the pond is half covered on the 29th day.

This gets even more exciting when applied to real life investing. Granted, finding an investment that doubles every day is tricky, but finding one that grows between 7-10% a year, not so much. This isn’t going to be another of the thousands of ‘compound interest is amazing’ posts available all over the internet, but allow me a quick example for noobs. If you invest a very modest £400 a month over 40 years, at an average 7% growth rate you’ll end up with £958,248.54.

Hopefully you’re suitably amazed, but where it gets difficult (and interesting) is getting humans to convert the knowledge into action. Anyone rational would read the above, fiddle with a compound interest calculator for an hour or so, the ‘I get it’ bell would ring in their head and they’d settle down into monthly investing for the long haul right?

I have a friend that has spent the last 20 years, skirting around the stocks/shares and lately crypto, trading world. Always hunting for that elusive ‘10 bagger’. Wanting an instant hit. Or, alternatively wishing that Amazon, or Facebook, or Nvidia or <insert your favourite success story here> shares had been bought and held. Despite this, apart from a house with a significant mortgage, no notable assets are owned. It’s all been spent on living a very good life. Holidays, travel, more holidays (a lot of holidays), eating out, cars, bikes and all the usual trappings of a middle class lifestyle. All of this despite having multiple friends that are habitual investors. All of this despite should you ask, willingly identifying the weaknesses that cause this behaviour. All of this despite wishing that more life options were available. You can lead a horse to water.

So back to the ‘very interesting if you’re Tim’ graph above. You can spot a combination of various life and stock market events. House purchase in 2007, a couple of dips around 2017/2018, covid crash 2020, the crypto crash in 2021 and the market decline in 2022, but despite all of that, the trend remains.

So good news for everyone reading. If you’re a slightly above average earner in the UK, if you have the stubborn persistency to just invest regularly no matter what noise the media is making at the time, the magic of compounding and exponential growth will happen and produce amazing results. Hopefully this gives you some inspiration to commit and tune out.

As an aside, you’ll notice that the 4% line has been crossed. For those that don’t know the significance, https://www.mrmoneymustache.com/2012/05/29/how-much-do-i-need-for-retirement/. Admittedly that 4% number hasn’t been adjusted for a couple of years, so might need an inflation tweak, but it was originally generous.

For the detail nerds, the net worth graphed here doesn’t include my final salary pension or house. I don’t include my house because I live in it. I don’t include my final salary pension to give further buffer. Maybe I’m slightly paranoid, but don’t count your chickens’n’all that.